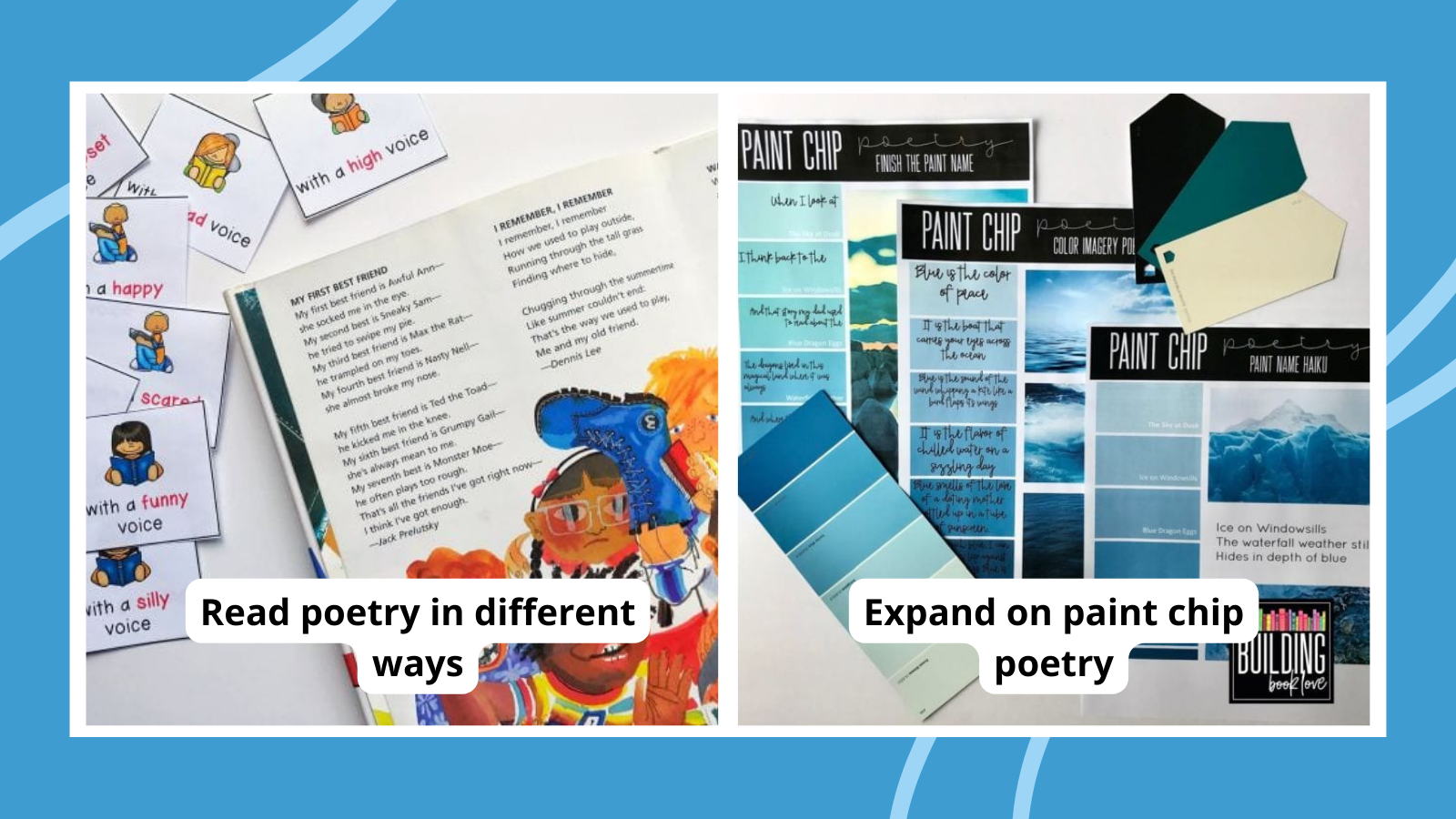

40 Inspiring Poetry Games and Activities for Kids and Teens

They are poets, and they know it!

27+ Best Autism Resources for Educators

Books, strategies, courses, and more.

Financial Literacy for Kids: Lessons, Activities, and Teaching Tips

Everyone needs to learn to manage their money.

Featured

Classroom Resources for Teaching Money Skills

Money-smart financial education lessons for K-12, brought to you by Hands on Banking, a public service provided by Wells Fargo.

Science Resources for Middle and High School

Free activities, videos, and articles that make teaching science easier—and more fun!

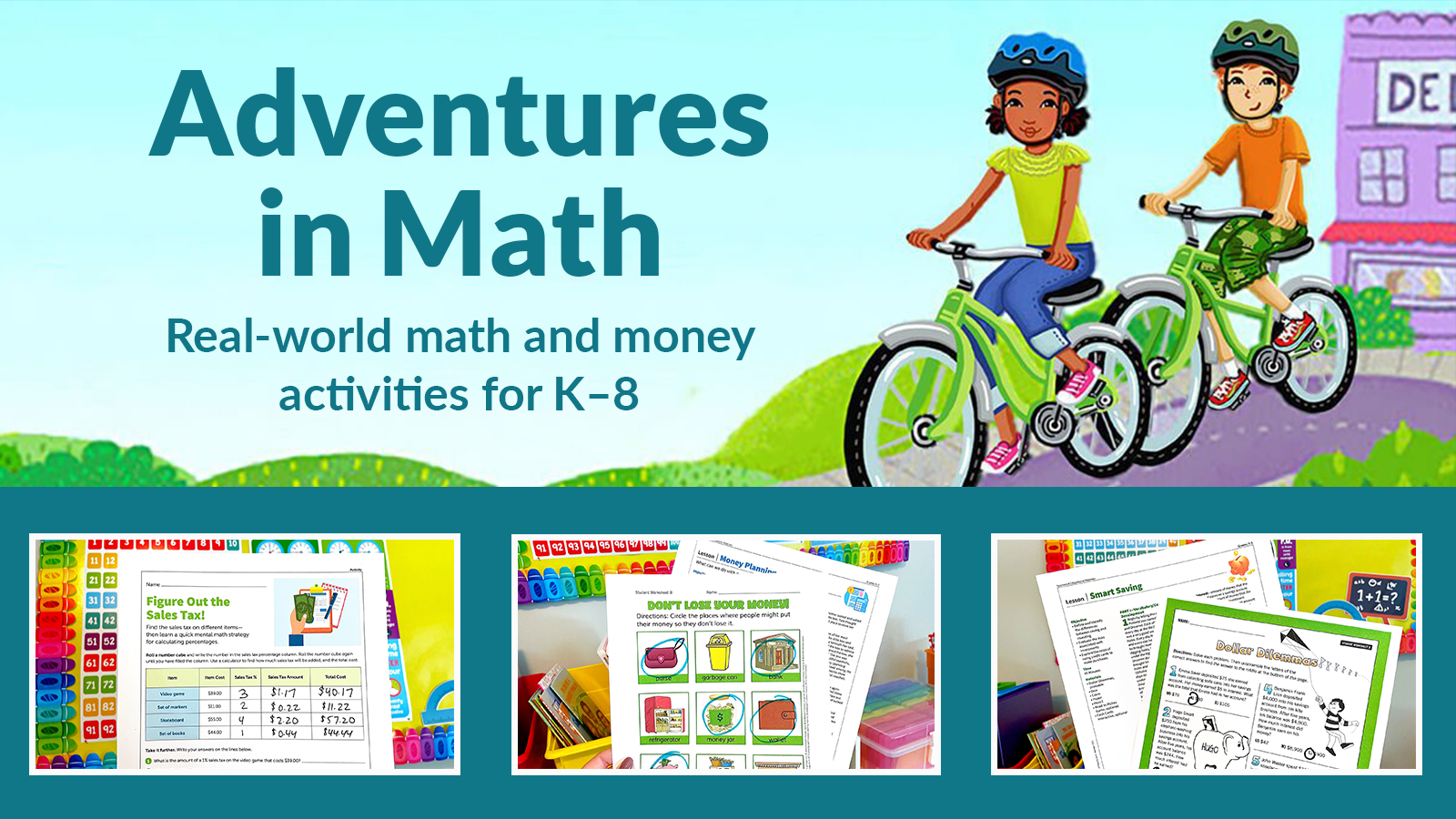

Adventures in Math

Real-world math and money activities for K–8. A free educational program to help teach kids math skills and financial responsibility.

Teach Your Students To Be Cyber Savvy

These lessons, activities, and games will boost your students’ STEM skills and get them ready to become the cyber detectives.

Top Stories

Get Our Free Spring Posters & Bring a Spot of Sunshine to Your Classroom

Hope, growth, and happiness.

Classroom Ideas

Browse by Topic

Discover classroom ideas, teaching strategies, and actionable tips for the subjects you teach every day.

Reading

Our top teacher-approved book lists, reading tips, and so much more!

Math

Find tips, resources, lesson plans, and games for K-12 that make math teachers’ lives easier.

Science

Science experiments, lesson plans, science themed books, and more!

Arts

Find everything from creative ideas for using music and theater at school to craft projects you’ll love.

ESL

Tips for English as a Second Language and English Language Learner teachers.

Social Studies

Economics, history, geography, sociology, anthropology, psychology … we have you covered.